If you don’t know what a customer is worth, you’re guessing

If you don’t know what a customer is worth to your business, every growth decision becomes a guess.

How much should you spend on marketing?

How much can you afford to pay for a lead?

How much should you reinvest into grow?

Most business owners don’t have clear answers.

Which is why they either play too small… or grow in a way that creates pressure on cash flow, delivery, or both.

This is where Customer Lifetime Value changes everything.

Not as a metric.

As a growth lever.

What is Customer Lifetime Value?

Customer Lifetime Value (CLV) is the total revenue a customer generates for your business over the entire relationship.

Simple example:

If a customer spends $3,000 with you over 3 years, their lifetime value is $3,000.

The CLV formula (simple version)

CLV = Average Purchase Value × Purchase Frequency × Customer Lifespan

| Metric | Example |

| Average job value | $500 |

| Jobs per year | 2 |

| Customer lifespan | 3 years |

| CLV | $3,000 |

Most business owners never do this, but the few that do stop here.

They calculate the number, then move on.

That’s where the real opportunity is missed.

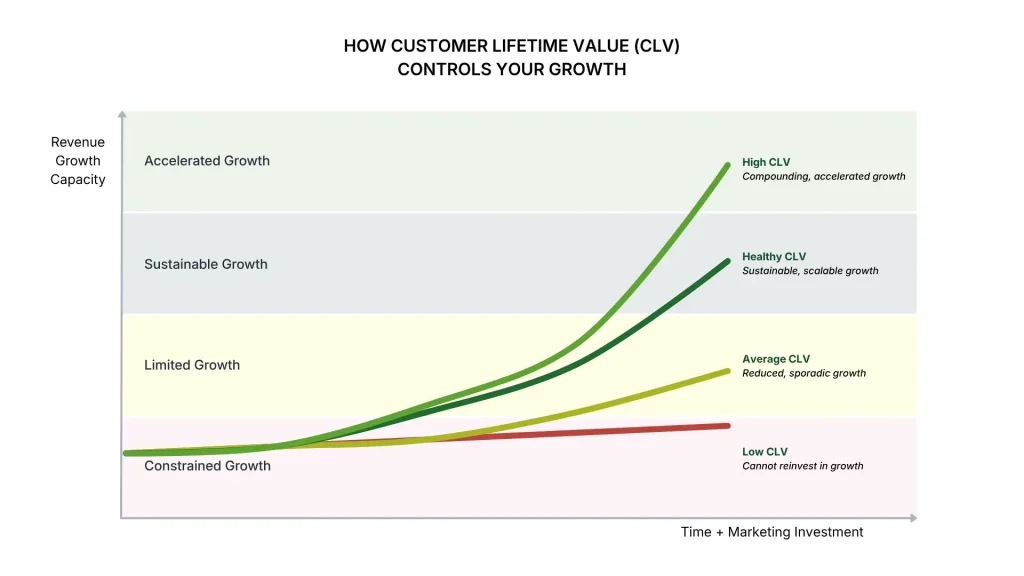

Why Customer Lifetime Value matters more than you think

1. It determines your marketing budget

The businesses that grow fastest are not always the best.

They are the ones that understand what a customer is worth and are willing to invest accordingly.

If your CLV is $5,000, spending $1,000 to acquire a customer makes sense.

If your CLV is $1,000, it doesn’t.

Growth goes to the business that can afford to invest the most to acquire a customer.

2. It shapes your growth strategy

High CLV gives you options.

- You can scale faster.

- You can outspend competitors.

- You can be more aggressive.

Low CLV forces you to play small.

Which is why many businesses feel stuck even when the initial demand exists.

3. It drives profitability

Customer acquisition cost is paid upfront. Profit is realised over time.

Most businesses focus on the cost today, but don’t fully understand how that customer's value is realised over time.

CLV is a system, not just a static number

Customer lifetime value is not something you calculate once.

It is something you design:

- Through your pricing

- Through your customer experience

- Through your follow-up

- Through your marketing

CLV is planned before the sale, but created after it.

You influence it through your pricing, your positioning, and the products and offers you bring to market.

But it’s ultimately determined by what happens after the customer first says yes.

- The experience you deliver.

- The way you communicate.

- The systems you have in place to stay in contact and bring them back.

That’s where lifetime value is either built… or lost.

CLV vs CAC: The ratio that controls your growth

What is CAC?

Customer Acquisition Cost (CAC) is what you spend to acquire a new customer.

Spend too much on acquisition and you lose money. Spend to little and you cap your growth. The trick is to find the right balance.

The 3:1 benchmark

| CLV:CAC Ratio | Meaning | Risk Level |

| 1:1 | Losing money | Unsustainable |

| 2:1 | Risky | Fragile growth |

| 3:1 | Healthy | Scalable |

| 5:1 | Likely under-investing | Missed growth opportunity |

| ∞ (no paid acquisition) | Dangerously under-investing | Hidden growth ceiling |

If you are not actively spending to acquire customers, your CLV:CAC ratio is technically infinite.

That might sound ideal... it isn’t.

It usually means your growth is left to chance rather than controlled by strategy.

What you should be aiming for

A practical benchmark to grow a service businesses is to being able to invest 25–33% of your customer lifetime value to acquire a new customer.

If your business cannot support that, one of two things is true:

- Your margins are too thin

- Your lifetime value is too low

The payback period problem

A healthy CLV does not guarantee a healthy business.

You might have:

CLV: $6,000

CAC: $2,000

Ratio: 3:1

On paper, that looks strong.

But if that value is realised over 10 years, you could be waiting years just to recover your acquisition cost.

For most service businesses, that is not sustainable.

This is where smart businesses step back and use strategic planning to shift their model.

They shorten the payback period by:

- Increasing upfront value

- Pre-selling future work

- Structuring offers to recover acquisition costs faster

In simple terms, they move toward what’s often called client-financed acquisition.

Where the customer funds their own acquisition through early-stage value.

Not all customer lifetime value is created the same

Recurring revenue businesses

These businesses grow CLV through retention.

The longer a customer stays, the more valuable they become.

The focus is simple:

- Reduce churn.

- Increase retention.

Service-based businesses

Most service businesses rely on one-off jobs, or a "churn-and-burn" model.

Which means CLV is often lower than it should be.

In reality, CLV is created through:

- Repeat work

- Referrals

- Additional services

If you're currently reliant on “one-off jobs,” your CLV is artificially capped.

How to increase customer lifetime value (without more leads)

Here are 6 practical ways to increase customer lifetime value in a service business.

1. Optimise the first experience

The first job sets the tone for everything that follows.

Being proactive, clear, and consistent in how you communicate often has more impact than marginal improvements in technical delivery.

And this is where many businesses get it wrong.

Your administration and customer-facing staff play a critical role in how your business is perceived. This includes:

- How calls are taken.

- How updates are communicated.

- How problems are explained.

- How complaints are handled.

Training, supporting and rewarding positive behaviours in these areas often provide one of the highest return-on-investments you can make.

Customers who feel heard are more likely to stay, spend more over time, and refer others.

Giving customers a structured way to provide feedback also builds trust and strengthens the relationship.

2. Pre-book future work

Nothing is worse than looking at a bare calendar a week or two from now.

One of the simplest ways to increase customer lifetime value is to secure the next job before the current one is finished.

If a customer hesitates, offer a small incentive:

“If you’d like to lock this in today, we can offer 10% off when you leave a deposit.”

This shifts the dynamic:

- From uncertain future work

- To guaranteed future revenue

You’ve effectively turned a “maybe” into a committed customer.

The second booking is often the turning point between a one-off customer and a long-term client.

3. Build follow-up systems

Most businesses rely on memory.

Successful, scalable businesses rely on systems.

Simple follow-up messages, reminders and check-ins keep your business top of mind without being intrusive.

The key is consistency without additional effort.

The most effective follow-up systems are built using a CRM (Customer Relationship Management tool) with email and SMS automation, to stay in contact with customers at the right time.

This might include:

- Service reminders

- Post-job check-ins

- Seasonal prompts

- Relevant offers based on past work

Once this is set up properly, it runs in the background and ensures no customer slips through the cracks.

It’s one of the simplest ways to increase repeat work without increasing your workload.

4. Leverage reviews and reputation

Trust accelerates everything.

Most business owners already know more reviews increase lead-flow. But that’s only a fraction of what reviews can do.

Reviews don’t just bring in more customers.

They influence the type of customers you attract.

Reviews build a stronger reputation and that naturally attracts:

- More decisive buyers

- Higher trust from the first interaction

- Customers who are less price-sensitive

And that improves the type of customer you win.

These customers enter the relationship expecting to have a good experience.

They are more open, more trusting and more likely to notice the positive aspects of your service.

They are also more likely to engage.

To give feedback.

To leave a review.

To recommend you to others.

There is often a social expectation at play as well. When customers choose a highly reviewed business, they are more inclined to contribute to that reputation themselves.

But there’s another layer.

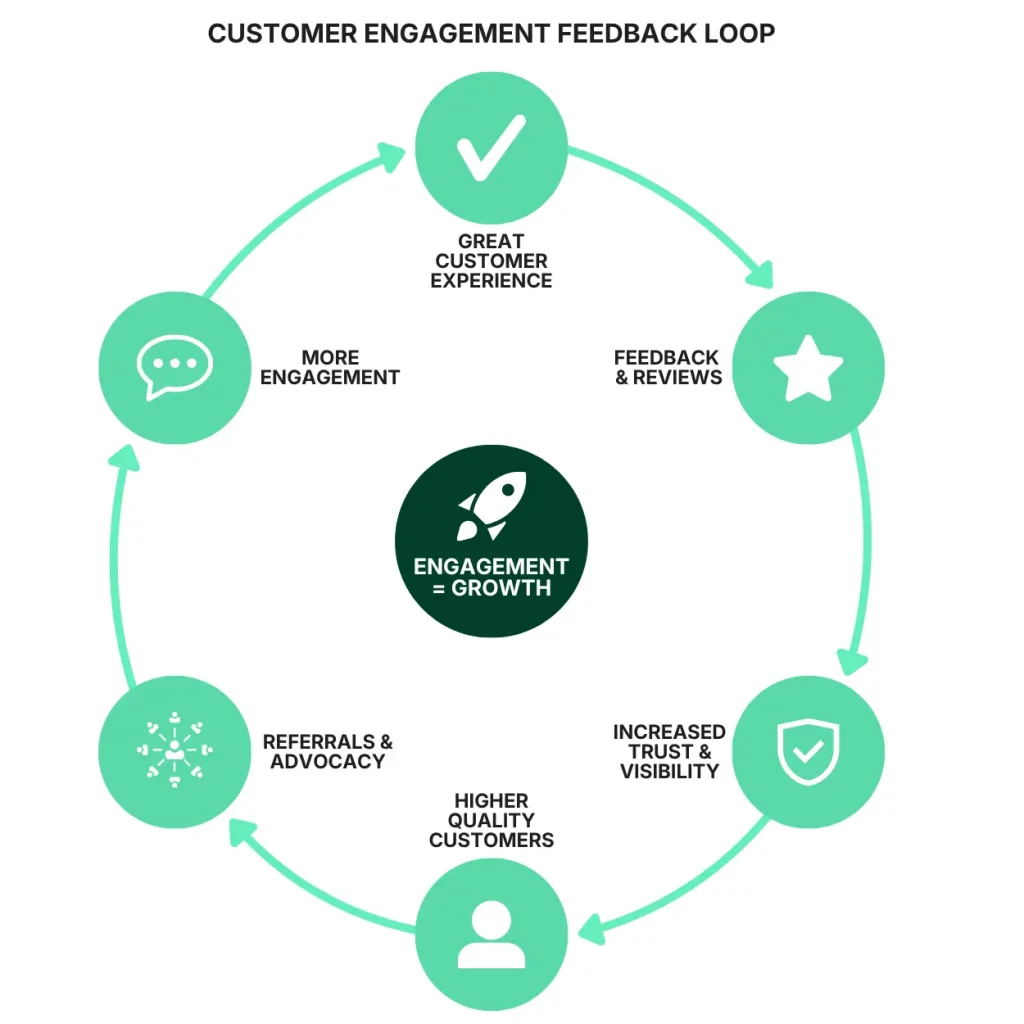

Customers who give feedback, leave reviews or refer others are more engaged.

And engaged customers are more valuable.

Customers who actively engage with a business by giving feedback, leaving reviews or referring others, generate 23% more revenue and profit over time than the average customer.

— Gallup

There’s also a psychological reason behind this.

When someone leaves a positive review, they are making a small public commitment.

And people naturally want to stay consistent with their own actions.

This is known as the Commitment and Consistency Principle, popularised by Robert Cialdini.

Once someone has publicly said, “this business is great,” they are more likely to:

Use you again

Recommend you to others

Publicly advocate for your business and influence others in your favour

In simple terms, reviews don’t just reflect a strong relationship.

Reviews strengthen the relationship.

And when you get more of your customers to leave reviews, it leads to:

- More repeat work

- More referrals

- A higher customer lifetime value.

The question is:

Are you getting reviews consistently… or leaving it to chance?

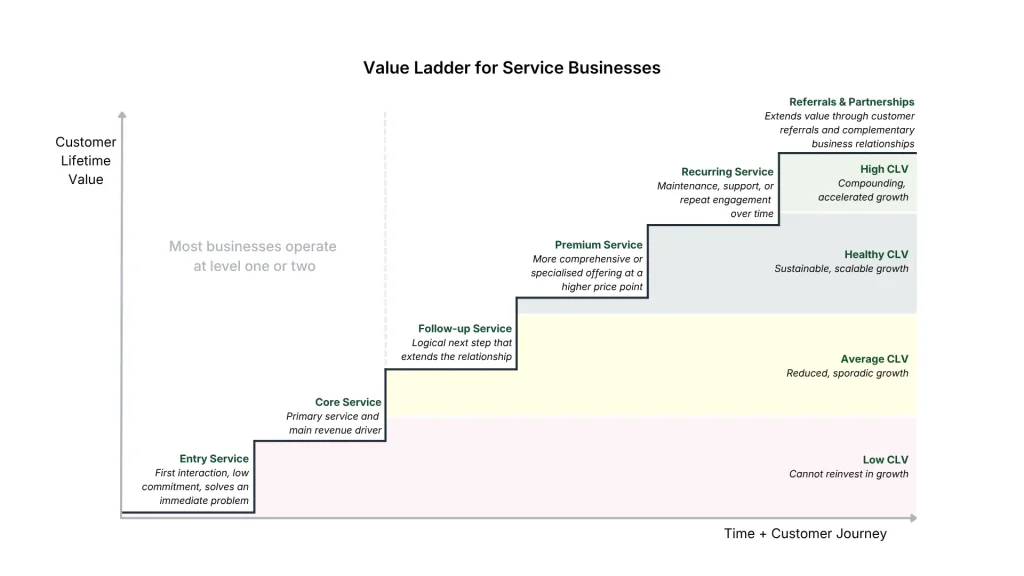

5. Create a value ladder

Most service businesses offer a series of one-off, parallel services.

A customer engages them for a single job on a project and that’s where the relationship ends.

Highly profitable businesses take a different approach.

They design a tiered progression of services and products, often referred to as a value ladder.

Instead of a single transaction, they create a pathway for customers to move through over time.

This shifts the relationship from one-off work to ongoing value.

And this is where lifetime value increases significantly.

Because once you’ve paid to acquire a customer, every additional service they purchase carries a much higher margin.

You’re no longer paying to win the customer again.

Which means more of that revenue goes straight to your bottom line.

A value ladder only works if you stay in contact with your customers.

As mentioned earlier, this is where simple follow-up systems become critical.

When you combine a clear value ladder with consistent follow-up, you create a scalable way to increase customer lifetime value without relying on memory or manual effort.

6. Build strategic partnerships

Strategic partnerships involve working with complementary, non-competing businesses that serve the same customer at different points in their journey.

There are two natural points where partnerships create value during a customer's journey:

1. During the customer relationship

At this stage, referrals enhance your service rather than replace it.

For example:

- A trades business referring a cleaner after a renovation

- An accountant referring a finance broker

- A physio referring a personal trainer

This improves the outcome for the customer and strengthens your position as a trusted provider.

2. At the end of your involvement

Every business reaches a point where it can no longer assist the customer.

At that point, the customer will either:

- Find another provider themselves

- Follow a trusted recommendation

When that recommendation comes from you, you stay part of the relationship rather than being replaced.

Why this increases customer lifetime value

Strategic partnerships don’t just help the customer. They improve your economics.

- Stronger trust leads to a higher likelihood of repeat work

- Better outcomes lead to more referrals

- Continued relationship leads to higher lifetime value

You’re not just completing a job.

You’re extending the relationship beyond it.

How partnerships are monetised

There are two common approaches.

| Model | How it works |

| Direct referral agreements | You receive a fee for connecting the customer to a trusted provider |

| Reciprocal partnerships | Both businesses consistently refer clients to each other |

In both cases, you increase the value of each customer without paying to acquire a new one.

Key takeaway

The goal is not to do everything for the customer.

It’s to become the business they trust to guide them.

Why customer lifetime value compounds over time

Retention drives profit

Increasing retention has a disproportionate impact on profitability.

Not because you’re doing more work. But because you’ve already paid to win the customer.

From that point on, every additional service, product or sale carries a much higher margin.

Which is why retention is one of the fastest ways to increase profit without increasing marketing spend.

The CLV growth loop

Referred customers:

- Trust you more

- Convert faster

- Stay longer

Because the trust has already been transferred.

Which means you spend less time convincing, and more time delivering.

That reduces your acquisition cost and increases the value of each customer.

Where customer lifetime value breaks down

Customer lifetime value breaks down when businesses miss the levers that actually drive it.

Here’s where it typically happens:

- They focus on getting more leads instead of increasing value per customer

- They ignore retention and follow-up

- They don’t understand their acquisition cost

- They treat every job as a one-off

- They fail to systemise the customer experience

These issues don’t always show up immediately.

But over time, they quietly cap your growth.

The question that determines how you grow

Customer Lifetime Value is not just a metric. It is the number that determines how aggressively your business can grow.

Most business owners are making that decision blind.

The question is not how many customers you can get. It’s "how much each customer is actually worth to your business" and "how can you increase their value further"?

Find out what’s actually holding your growth back

Without clear answers to these questions, most businesses don’t know where their quickest wins are.

- They don’t know which lever to pull first.

- They don’t know which change will have the biggest impact.

- And they don’t know what’s quietly limiting their growth.

That’s why we created the Business Growth Scorecard.

It’s an AI-powered diagnostic, built on real-world business growth frameworks, designed to give you the clarity of a $1,000 consulting session in under three minutes, without needing to speak to anyone.

Once complete, you’ll know:

- Where your biggest growth constraints are

- Which levers will have the fastest impact

- What to prioritise to increase revenue and profit

- How to start building a business that can grow without relying on you

In less than 3 minutes, it will help you identify where you’re stuck, what’s causing it and what to focus on next.

No guesswork.

Just a clearer path forward.